The Role of Blockchain in Enhancing the Global Digital Economy is no longer a futuristic fantasy; it’s a rapidly unfolding reality. This revolutionary technology, with its decentralized, immutable ledger, is reshaping finance, supply chains, and digital identity management on a global scale. From streamlining cross-border payments to bolstering intellectual property rights, blockchain’s impact is profound and far-reaching, promising a more secure, transparent, and efficient digital world. But it’s not all sunshine and rainbows; we’ll explore the challenges and opportunities that lie ahead in this exciting, ever-evolving landscape.

Imagine a world where financial transactions happen instantly and securely across borders, supply chains are completely transparent, and your digital identity is truly yours to control. That’s the potential of blockchain. We’ll dive into the specifics, looking at real-world applications and addressing the hurdles that need to be overcome for widespread adoption. Get ready to unlock the potential of this game-changing technology.

Blockchain Technology Fundamentals

Blockchain technology is revolutionizing how we think about data management and security. It’s more than just a buzzword; it’s a foundational technology with the potential to reshape entire industries, and its impact on the global digital economy is already being felt. Understanding its core principles is crucial to grasping its transformative power.

At its heart, blockchain is a distributed ledger technology (DLT). Imagine a digital record book shared among many computers (nodes) across a network. Every transaction is recorded as a “block” and added to this chain, creating an immutable, chronological record. This differs drastically from traditional centralized databases controlled by a single entity.

Decentralization, Immutability, and Distributed Ledger Technology

These three pillars are the bedrock of blockchain’s strength. Decentralization means no single entity controls the blockchain; it’s spread across a network, making it highly resistant to censorship and single points of failure. Immutability ensures that once a block is added to the chain, it cannot be altered or deleted, guaranteeing data integrity. The distributed ledger aspect means multiple copies of the blockchain exist, enhancing security and reliability. If one node fails, the others continue to operate, maintaining the system’s functionality. This contrasts sharply with centralized databases, where a single point of failure can cripple the entire system.

Blockchain’s secure, transparent nature is revolutionizing the global digital economy, impacting everything from finance to supply chains. This decentralized tech even extends to the smart home revolution, as seen in how data security and automation are enhanced in How Smart Homes are Redefining Modern Living. Ultimately, blockchain’s potential to secure and streamline data exchange will further accelerate the growth of the interconnected digital world, including the ever-evolving smart home landscape.

Blockchain Architectures: Public, Private, and Consortium

Different blockchain architectures cater to various needs and levels of access control. The choice of architecture depends on the specific application and the desired level of transparency and permissioning.

Public blockchains, like Bitcoin, are open to anyone. Transactions are transparent and verifiable by all participants. Private blockchains, on the other hand, are permissioned; access is restricted to authorized users or organizations. Consortium blockchains represent a hybrid approach, with access controlled by a pre-selected group of organizations. Each architecture offers a unique balance between transparency, security, and control.

Blockchain vs. Traditional Centralized Databases

The core difference lies in the approach to data management and control. Centralized databases rely on a single authority to manage and control data, making them vulnerable to single points of failure, data breaches, and manipulation. Blockchains, with their decentralized and immutable nature, offer enhanced security, transparency, and resilience.

| Feature | Blockchain | Centralized Database |

|---|---|---|

| Data Storage | Distributed across a network | Centralized server |

| Data Security | High, due to cryptography and decentralization | Vulnerable to single points of failure and hacking |

| Transparency | High (in public blockchains) | Limited, controlled by the central authority |

| Immutability | High | Mutable; data can be altered or deleted |

Advantages and Disadvantages of Blockchain Technology

Like any technology, blockchain has its pros and cons. Its global impact hinges on effectively leveraging its strengths while mitigating its weaknesses.

| Advantages | Disadvantages |

|---|---|

| Enhanced Security and Transparency | Scalability challenges; transaction speeds can be slow |

| Increased Efficiency and Reduced Costs | Regulatory uncertainty and lack of standardization |

| Improved Trust and Data Integrity | High energy consumption (particularly with proof-of-work consensus mechanisms) |

| Greater Data Control and Privacy (in private blockchains) | Complexity and technical expertise required for implementation |

Blockchain’s Impact on Global Finance: The Role Of Blockchain In Enhancing The Global Digital Economy

The global financial system, despite its sophistication, still faces significant hurdles. High transaction fees, slow processing times, and a lack of transparency plague cross-border payments. This is where blockchain technology steps in, promising a revolution in how we handle money on a global scale. Its decentralized, secure, and transparent nature offers solutions to many long-standing problems, potentially reshaping the financial landscape for individuals and businesses alike.

Blockchain’s potential to transform global finance is vast, impacting everything from international remittances to access to financial services in underserved communities. This transformative power stems from its core features: immutability, transparency, and security, all of which contribute to a more efficient and trustworthy financial ecosystem.

Cross-Border Payments and Remittances

Cross-border payments often involve multiple intermediaries, leading to delays and hefty fees. Blockchain streamlines this process by enabling direct, peer-to-peer transactions. Instead of relying on traditional banking networks, individuals and businesses can transfer funds quickly and cheaply using blockchain-based platforms. This is particularly beneficial for migrant workers sending remittances to their families in their home countries, as they can avoid the exorbitant fees charged by traditional money transfer services. For example, Ripple’s xRapid network utilizes blockchain to facilitate faster and cheaper cross-border payments, reducing the reliance on correspondent banks and streamlining the process. The transparency offered by blockchain also increases accountability, making it easier to track transactions and reduce fraud.

Blockchain and Financial Inclusion in Developing Countries

Millions worldwide lack access to traditional banking services, hindering economic growth and opportunity. Blockchain technology can play a vital role in extending financial services to these underserved populations. Mobile money platforms built on blockchain can provide access to basic financial services like savings accounts, microloans, and insurance, even in areas with limited infrastructure. For instance, several projects in Africa are leveraging blockchain to create accessible and affordable financial services for unbanked communities, empowering them to participate more fully in the economy. This increased access to financial services can stimulate economic activity and improve livelihoods.

Blockchain-Based Financial Applications: Stablecoins and Decentralized Finance (DeFi)

The rise of stablecoins and decentralized finance (DeFi) showcases blockchain’s innovative potential in the financial sector. Stablecoins, cryptocurrencies pegged to a stable asset like the US dollar, aim to mitigate the volatility inherent in many cryptocurrencies. They offer a more stable medium of exchange for online transactions and can facilitate cross-border payments with reduced risk. DeFi, on the other hand, encompasses a range of financial applications built on blockchain, including lending, borrowing, and trading, without relying on intermediaries like banks. These applications can provide access to financial services that are more efficient and transparent, potentially democratizing finance. MakerDAO’s DAI is a prominent example of a stablecoin, while platforms like Aave and Compound illustrate the growing potential of DeFi.

A Hypothetical Scenario: Enhancing International Trade Finance

Imagine a scenario involving the export of goods from a small business in Vietnam to a buyer in the United States. Traditionally, this process would involve multiple banks, letters of credit, and extensive documentation, leading to delays and high costs. With blockchain, the entire process could be streamlined. A smart contract, a self-executing contract written in code and stored on the blockchain, could automate the release of payment upon verification of shipment and delivery. This would eliminate the need for intermediaries, reducing costs and speeding up the process. Furthermore, the immutable record on the blockchain would provide transparency and security, reducing the risk of fraud and disputes. This hypothetical scenario showcases how blockchain can enhance security and efficiency in international trade finance, fostering greater trust and collaboration between trading partners.

Blockchain and Supply Chain Management

Source: extnoc.com

Forget endless spreadsheets and confusing paperwork. Blockchain is revolutionizing supply chains, offering a level of transparency and traceability previously unimaginable. By leveraging its immutable ledger technology, businesses can track products from origin to consumer with unprecedented accuracy, boosting efficiency and building trust with customers. This section explores how blockchain enhances various aspects of global supply chain management.

Improved Transparency and Traceability in Global Supply Chains

Blockchain’s decentralized and transparent nature offers a significant advantage in global supply chains. Each transaction and movement of goods is recorded on the blockchain, creating an auditable trail that can be accessed by all authorized parties. For example, imagine tracking a shipment of mangoes from a farm in Thailand to a supermarket in the US. Using blockchain, every step – from harvesting and packaging to transportation and storage – can be recorded and verified, eliminating the possibility of data manipulation or discrepancies. This increased transparency allows businesses to identify bottlenecks, optimize logistics, and respond quickly to potential issues. Another example involves pharmaceuticals; tracking drugs through the supply chain helps ensure authenticity and prevent counterfeit products from entering the market, safeguarding public health.

Challenges Associated with Implementing Blockchain in Complex Supply Chain Networks

While the potential benefits are substantial, implementing blockchain in complex supply chains presents several challenges. Integration with existing legacy systems can be costly and time-consuming. Achieving consensus among multiple stakeholders across different organizations requires careful coordination and agreement on data standards and protocols. Furthermore, the scalability of blockchain technology needs to be considered, particularly for large-scale supply chains involving millions of transactions. Finally, ensuring data privacy and security while maintaining transparency is a delicate balancing act. For example, while tracking coffee beans from farm to cup is beneficial, the specific farmer’s location might need to be protected for privacy reasons.

Enhanced Security and Authenticity of Products Throughout the Supply Chain

Blockchain’s cryptographic security features make it incredibly difficult to tamper with data, ensuring the authenticity and integrity of products throughout the supply chain. Each product can be assigned a unique digital identity, allowing for easy verification of its origin and journey. This is especially crucial for luxury goods, pharmaceuticals, and food products, where counterfeiting is a major concern. For instance, a high-end watch could have its entire production history recorded on the blockchain, verifying its authenticity and provenance. Similarly, tracking food products allows consumers to verify their origin and quality, reducing the risk of foodborne illnesses linked to contaminated or mislabeled goods.

Step-by-Step Integration of Blockchain into a Global Coffee Bean Supply Chain

Let’s consider a hypothetical global supply chain for coffee beans, from farm to consumer.

- Farm-Level Tracking: Farmers record details about their coffee bean harvest, including variety, quantity, and environmental conditions, directly onto the blockchain using a mobile app.

- Processing and Export: Once processed, the coffee beans are packaged, and the details are updated on the blockchain, including weight, processing methods, and export information.

- Transportation and Logistics: Shipping and handling information is added to the blockchain at each stage of transportation, providing real-time tracking and visibility.

- Roasting and Packaging: Roasters add details about their roasting process and packaging information to the blockchain.

- Retail and Consumer Access: Consumers can scan a QR code on the coffee packaging to access the complete history of the beans, from farm to their cup, building trust and transparency.

This step-by-step process ensures complete traceability and transparency, empowering consumers with detailed information about the product’s journey and fostering greater trust in the supply chain.

Blockchain’s Role in Digital Identity and Data Management

The digital age has ushered in an era of unprecedented data generation and interconnectedness. However, this explosion of information also presents significant challenges regarding security, privacy, and control. Traditional centralized systems for managing digital identities and personal data are proving increasingly vulnerable to breaches and misuse. Blockchain technology, with its inherent security and transparency, offers a compelling alternative, promising a more secure and user-centric approach to digital identity and data management.

Blockchain’s decentralized and immutable nature makes it uniquely suited to address the shortcomings of centralized systems. By distributing identity information across a network, blockchain mitigates the risk of single points of failure and enhances resilience against cyberattacks. Furthermore, its cryptographic security ensures the integrity and authenticity of digital identities, fostering trust and enabling secure interactions in the global digital economy.

Secure and Verifiable Digital Identities

Blockchain technology enables the creation of self-sovereign digital identities. Instead of relying on a single authority to verify and manage identity information, individuals gain control over their own data. This is achieved through the use of cryptographic techniques that allow individuals to prove their identity without revealing sensitive personal information. For example, a user might prove their age without disclosing their exact birthdate, or verify their employment status without revealing their full employment history. This approach significantly improves privacy while still allowing for secure verification. Consider a scenario where a user needs to prove their identity to access a service; with a blockchain-based identity system, they can selectively share only the necessary information, maintaining greater control over their personal data.

Enhanced Data Privacy and Security

Blockchain enhances data privacy and security through several mechanisms. Data encryption ensures that only authorized parties can access sensitive information. The immutability of the blockchain prevents unauthorized alteration or deletion of data, providing a tamper-proof record of identity and transactions. Furthermore, access control mechanisms can be implemented to restrict access to specific data elements based on predefined rules. This granular control over data access minimizes the risk of data breaches and unauthorized disclosures. Imagine a healthcare system utilizing blockchain to manage patient records. Doctors could access relevant information, while maintaining patient confidentiality through controlled access rights, thereby significantly enhancing data security and privacy.

Comparison of Blockchain-Based and Traditional Identity Systems

Traditional centralized identity systems rely on a single entity (e.g., a government or a company) to manage and control all identity information. This creates a single point of failure, making the system vulnerable to hacking and data breaches. In contrast, blockchain-based systems distribute identity information across a network, eliminating the single point of failure and enhancing resilience. Moreover, blockchain systems empower individuals with greater control over their own data, enabling them to selectively share information as needed, a feature largely absent in traditional systems. The privacy implications are also starkly different; centralized systems often collect and store vast amounts of personal data, potentially leading to misuse, while blockchain-based systems can prioritize privacy by design.

Potential Applications of Blockchain for Managing Personal Data

The potential applications of blockchain for managing personal data in a globally interconnected environment are vast and transformative.

- Secure online voting: Blockchain can ensure the integrity and transparency of online voting systems, preventing fraud and manipulation.

- Digital diplomas and certificates: Institutions can issue verifiable digital credentials on a blockchain, making it easier for individuals to prove their qualifications.

- Supply chain traceability: Tracking the movement of goods and materials throughout the supply chain, ensuring authenticity and provenance.

- Cross-border identity verification: Facilitating secure and efficient identity verification for international travel and transactions.

- Decentralized data marketplaces: Allowing individuals to control and monetize their own data.

Blockchain and Intellectual Property Rights

The digital age has revolutionized how we create, share, and protect intellectual property. Traditional methods struggle to keep pace with the speed and scale of digital content distribution, leaving creators vulnerable to infringement. Blockchain technology, with its immutable ledger and cryptographic security, offers a powerful new tool for safeguarding intellectual property rights globally, providing a transparent and secure system for managing digital assets.

Blockchain’s decentralized and transparent nature makes it ideal for registering and verifying ownership of digital assets. By recording ownership details on a blockchain, creators can establish a verifiable chain of custody, proving their ownership and preventing unauthorized use. This creates a stronger legal foundation for enforcing intellectual property rights and significantly reduces the challenges associated with proving ownership in disputes.

Blockchain’s Impact on Digital Asset Ownership Registration and Verification

Blockchain offers a robust solution for registering and verifying ownership of digital assets, including software, music, artwork, and literary works. Each asset can be assigned a unique digital fingerprint or token, representing its ownership. This token, recorded on the blockchain, serves as irrefutable proof of ownership, accessible to all authorized parties. This transparent system minimizes disputes and significantly streamlines the process of verifying ownership. For example, a musician could register their song’s unique digital fingerprint on a blockchain, providing irrefutable proof of their creation and ownership. This record remains tamper-proof, creating a secure and verifiable history of ownership.

Preventing Counterfeiting and Piracy of Digital Content Using Blockchain

The immutable nature of blockchain technology makes it extremely difficult to alter or delete records of ownership. This characteristic directly addresses the challenges of counterfeiting and piracy. By tracking the digital fingerprint of an asset across its lifecycle, blockchain can effectively identify and flag counterfeit copies or unauthorized reproductions. Imagine a system where every copy of a digital artwork is linked to its original blockchain record. Any attempt to distribute an unauthorized copy would be immediately identifiable through discrepancies in the digital fingerprint. This provides a powerful deterrent against piracy and significantly strengthens copyright protection. Furthermore, smart contracts can be programmed to automatically enforce licensing agreements, further preventing unauthorized distribution and use.

A System for Tracking Ownership and Licensing of Digital Artwork Across International Borders

A blockchain-based system for tracking digital artwork could involve several key components. First, each artwork would be assigned a unique digital identifier, linked to a blockchain record containing details such as the artist’s identity, creation date, ownership history, and licensing agreements. This record would be cryptographically secured and tamper-proof. The system would facilitate the secure transfer of ownership through smart contracts, automatically updating the blockchain record with each transaction. International transactions would be simplified by the system’s transparency and global accessibility, eliminating the need for complex cross-border legal processes. This system could be further enhanced by integrating with existing intellectual property registries, creating a unified and globally accessible database of digital artwork ownership. For example, an artist selling their artwork through an online marketplace could use this system to securely transfer ownership and licensing rights to the buyer, with the entire transaction recorded on the blockchain for complete transparency and auditability. This creates a trustless environment where both the buyer and seller can have confidence in the legitimacy of the transaction, regardless of their geographical location.

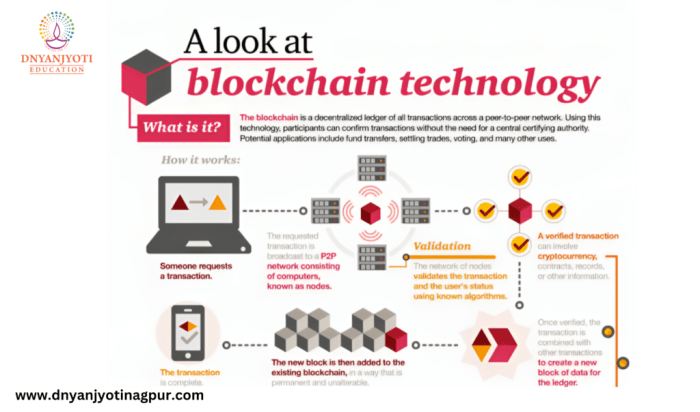

Challenges and Opportunities in Global Blockchain Adoption

Source: dnyanjyotinagpur.com

The global adoption of blockchain technology, while brimming with potential, faces significant hurdles. Navigating these challenges requires a multifaceted approach, encompassing regulatory reform, technological advancements, and a careful consideration of ethical implications. Only then can we fully unlock the transformative power of blockchain for the global digital economy.

Regulatory Hurdles and Legal Challenges

The decentralized and often anonymous nature of blockchain presents significant challenges for regulators worldwide. Existing legal frameworks, designed for centralized systems, struggle to adapt to the unique characteristics of blockchain. For instance, issues surrounding taxation of cryptocurrency transactions, the classification of cryptocurrencies as securities or commodities, and the enforcement of contracts on decentralized platforms remain largely unresolved in many jurisdictions. The lack of a unified global regulatory framework creates uncertainty and hinders investment, stifling innovation and potentially leading to regulatory arbitrage, where businesses operate in jurisdictions with the most lenient rules. This fragmentation necessitates international cooperation to establish clear, consistent, and adaptable regulations that promote innovation while mitigating risks.

Interoperability and Standardization Needs

The current blockchain ecosystem is fragmented, with numerous competing platforms and protocols lacking interoperability. This limits the scalability and efficiency of blockchain applications. For instance, a supply chain solution built on one blockchain might not seamlessly integrate with another used by a different partner, creating bottlenecks and hindering widespread adoption. Standardization efforts are crucial to address this issue. The development of common protocols and data formats will facilitate seamless data exchange between different blockchain networks, enhancing efficiency and promoting wider adoption across various sectors. This interoperability is essential for the creation of a truly global, interconnected digital economy powered by blockchain.

Ethical Considerations in Global Blockchain Use, The Role of Blockchain in Enhancing the Global Digital Economy

The ethical implications of blockchain technology are complex and far-reaching. Concerns regarding data privacy, algorithmic bias, and the potential for misuse in areas such as surveillance and censorship need careful consideration. The transparency of blockchain, while beneficial in many contexts, can also expose sensitive information if not properly managed. Furthermore, the decentralized nature of some blockchain platforms can make it difficult to hold actors accountable for malicious activities or unethical practices. Establishing robust ethical guidelines and developing mechanisms for accountability are crucial to ensuring the responsible and beneficial use of blockchain technology globally. This includes promoting transparency, fostering user education, and developing mechanisms for redress in case of ethical violations.

A Potential Future Scenario: Blockchain’s Widespread Adoption

Imagine a future where blockchain underpins the global digital economy. Supply chains are transparent and traceable, reducing fraud and counterfeiting. Digital identities are secure and self-sovereign, empowering individuals with greater control over their personal data. Intellectual property rights are protected more effectively, fostering innovation. Financial transactions are faster, cheaper, and more secure. However, this future is not without its challenges. The potential for increased surveillance and the concentration of power in the hands of a few large blockchain platforms are significant risks. Furthermore, the digital divide could widen, as access to blockchain technology and its benefits may not be equally distributed across the globe. This scenario highlights the need for proactive measures to address these potential negative consequences, ensuring a future where blockchain enhances the global digital economy equitably and sustainably. A successful integration will require robust regulatory frameworks, technological advancements that enhance scalability and interoperability, and a strong ethical foundation to guide its development and deployment.

Wrap-Up

Blockchain technology is poised to revolutionize the global digital economy, offering solutions to long-standing problems in finance, supply chain management, and data security. While challenges remain – regulatory hurdles, interoperability issues, and ethical considerations – the potential benefits are undeniable. As we move forward, navigating these challenges and fostering collaboration will be key to unlocking the full transformative power of blockchain and building a more secure, transparent, and inclusive digital future. The journey is just beginning, and the possibilities are limitless.