How Blockchain is Enabling Trust in Digital Transactions? Forget shady dealings and handshakes – blockchain’s shaking up the digital world, one secure transaction at a time. Imagine a system where every transaction is transparent, tamper-proof, and verifiable by anyone. That’s the promise of blockchain, a revolutionary technology that’s building trust where it was previously lacking. This isn’t just about crypto; it’s about transforming how we handle everything from supply chains to online payments, creating a more secure and efficient future.

From its decentralized nature to its cryptographic security, blockchain offers a compelling alternative to traditional systems. This deep dive explores how this technology works, its benefits, challenges, and its potential to reshape our digital interactions, ultimately making the online world a safer and more trustworthy place. We’ll explore how immutability and transparency are its cornerstones, and how smart contracts are automating trust like never before.

Introduction to Blockchain and Digital Transactions

Blockchain technology is revolutionizing how we conduct digital transactions, offering a level of trust previously unattainable in many online interactions. It’s a decentralized, distributed ledger that records and verifies transactions across a network of computers. This means no single entity controls the data, enhancing security and transparency. Understanding its fundamental concepts is key to grasping its impact on trust.

Blockchain’s core innovation lies in its structure: a chain of blocks, each containing a batch of verified transactions. These blocks are cryptographically linked, creating an immutable record. Any attempt to alter a past transaction would break the chain and be immediately detectable by the network. This inherent security feature differentiates it significantly from traditional databases.

Blockchain versus Traditional Databases

Traditional databases, often centralized and controlled by a single entity, are vulnerable to manipulation and single points of failure. A hacker breaching a central server could compromise all the data. Blockchain, on the other hand, distributes the data across numerous computers, making it far more resilient to attacks. This decentralization also eliminates the need for a trusted third party to verify transactions, a process that often introduces delays and costs.

Examples of Digital Transactions Requiring High Trust

Numerous digital transactions rely heavily on trust. Consider online banking: you trust your bank to securely process your payments and protect your financial information. Similarly, cryptocurrency transactions depend on the blockchain’s integrity to ensure the validity of digital asset transfers. Supply chain management benefits from blockchain’s transparency, allowing companies to track products from origin to consumer, verifying authenticity and ethical sourcing. Digital identity verification leverages blockchain to create secure and tamper-proof digital identities. The secure transfer of medical records and intellectual property rights are further examples where trust is paramount.

Comparison of Transaction Methods

The following table compares traditional and blockchain-based transaction methods across key aspects:

| Method | Security | Transparency | Cost |

|---|---|---|---|

| Traditional Database (e.g., bank transfer) | Relies on centralized security measures, vulnerable to single points of failure. | Limited transparency; only parties involved have access to full transaction details. | Potentially high transaction fees due to intermediaries. |

| Blockchain-based (e.g., cryptocurrency transaction) | Decentralized and highly secure due to cryptographic hashing and distributed ledger. | High transparency; all transactions are publicly viewable (though identities may be pseudonymous). | Transaction fees vary but can be lower than traditional methods in some cases. |

Immutability and Transparency in Blockchain

Blockchain technology’s revolutionary impact on digital transactions stems largely from its inherent immutability and transparency. These two features work in tandem to foster trust in a system traditionally vulnerable to manipulation and fraud. By understanding how they function, we can appreciate the profound shift blockchain represents in the digital landscape.

Immutability, the inability to alter or delete data once it’s recorded, is the bedrock of blockchain’s trustworthiness. This characteristic contrasts sharply with traditional databases, where information can be easily modified, potentially leading to discrepancies and fraud. Transparency, on the other hand, ensures that all transactions are visible to participants on the network, promoting accountability and deterring malicious activity. Together, immutability and transparency create a secure and verifiable record of all transactions.

Immutability’s Role in Building Trust

The immutable nature of blockchain creates a highly reliable and trustworthy system. Because each block is cryptographically linked to the previous one, any attempt to alter a past transaction would require altering the entire chain, a computationally infeasible task given the distributed and secured nature of the network. This inherent resistance to tampering builds confidence among users, as they know the history of transactions is permanently etched and verifiable. Think of it like a tamper-evident seal, but on a massive, decentralized scale. This significantly reduces the risk of data manipulation and ensures the integrity of the records.

Transparency Enhances Accountability in Transactions

Blockchain’s transparency mechanism works by making all transactions publicly viewable (depending on the specific blockchain’s design; some allow for pseudonymous transactions). Every participant can see the details of each transaction, fostering a level of accountability that is unprecedented in many traditional systems. This openness allows for easy auditing and verification of transactions, making it difficult for individuals or organizations to engage in fraudulent activities without detection. The public nature of the ledger acts as a powerful deterrent, as any attempt at manipulation would be immediately apparent to all network participants.

Examples of Blockchain Transparency Preventing Fraud

Consider the supply chain industry. Using blockchain, companies can track products from origin to consumer, ensuring authenticity and preventing counterfeiting. Each step in the supply chain, from raw material sourcing to final sale, is recorded on the blockchain, making it transparent and traceable. If a product is found to be counterfeit, the entire history of its journey can be easily examined, identifying the point of origin of the fraudulent activity. Similarly, in the financial sector, blockchain can be used to track the movement of funds, making it easier to identify and prevent money laundering and other financial crimes. The transparency provided by the blockchain allows for real-time monitoring and detection of suspicious activities.

Hypothetical Scenario Demonstrating Immutability, How Blockchain is Enabling Trust in Digital Transactions

Imagine a company using blockchain to record its employee payroll. Let’s say an employee’s salary is mistakenly recorded as $100 instead of $1000. In a traditional database, this error could be easily corrected, potentially without leaving a trace. However, on a blockchain, this erroneous record becomes a permanent part of the chain. To correct it, the company would need to create a new transaction that reverses the initial payment and then creates a new, correct payment. This process creates a clear and auditable record of the correction, ensuring transparency and preventing any attempts to cover up the initial error. The original incorrect record remains visible, creating a complete and verifiable history of the transaction. This demonstrates how immutability protects against unintentional errors and deliberate attempts to alter data.

Decentralization and its Impact on Trust

Imagine a world where your financial transactions aren’t controlled by a single entity, a bank, or a government. That’s the power of decentralization in blockchain. It’s a fundamental shift from traditional systems, profoundly impacting how we trust digital interactions. This section explores the concept of decentralization and how it fosters trust in the digital realm.

Decentralization in blockchain means that no single entity controls the network. Instead, the network is distributed across many computers (nodes) worldwide. Each node maintains a copy of the blockchain, ensuring redundancy and resilience. This distributed ledger technology makes it incredibly difficult for any single actor to manipulate or control the data. This contrasts sharply with centralized systems, where a single point of control exists, creating a single point of failure and vulnerability.

Centralized versus Decentralized Systems: A Trust Comparison

Centralized systems, like traditional banking, rely on trust in a central authority. This authority, be it a bank or a government, validates and records transactions. While convenient, this approach creates a single point of failure: if the central authority is compromised, the entire system is at risk. Trust is placed solely in the integrity and security of this single entity. Decentralized systems, on the other hand, distribute trust. No single entity holds ultimate control; the network itself ensures the integrity of the data through cryptographic hashing and consensus mechanisms. This makes the system far more resistant to manipulation and failure.

Advantages of Decentralization in Ensuring Trust

Decentralization offers several key advantages in building trust within digital transactions. The distributed nature of the network makes it incredibly resilient to attacks. Even if some nodes are compromised, the majority of the network continues to function, maintaining the integrity of the blockchain. Furthermore, the transparency inherent in blockchain technology allows anyone to verify transactions, fostering accountability and reducing the potential for fraud. The immutability of the blockchain, once a transaction is recorded, it cannot be altered or deleted, further reinforces trust. This creates a verifiable and auditable record of all transactions.

Benefits of Decentralization for Digital Transactions

The benefits of decentralization extend beyond simply increasing trust. It also enhances:

- Security: Distributed ledger technology makes the system more resistant to hacking and data breaches.

- Transparency: All transactions are publicly verifiable, increasing accountability and reducing fraud.

- Efficiency: Automated processes and reduced reliance on intermediaries streamline transactions.

- Resilience: The network’s distributed nature makes it resistant to single points of failure.

- Accessibility: Anyone with an internet connection can participate in the network.

For example, the use of blockchain in supply chain management allows for greater transparency and traceability of goods, building trust among consumers and businesses. Knowing the exact origin and journey of a product increases confidence in its authenticity and quality. Similarly, decentralized finance (DeFi) applications are leveraging blockchain to offer financial services without the need for traditional intermediaries, fostering greater financial inclusion and reducing reliance on centralized institutions. These real-world applications demonstrate the transformative potential of decentralization in building trust and enhancing efficiency in the digital economy.

Cryptographic Security in Blockchain Transactions

Blockchain technology wouldn’t be nearly as revolutionary as it is without its robust security features. At its core, blockchain’s trustworthiness hinges on sophisticated cryptographic mechanisms that safeguard the integrity and authenticity of every transaction. These methods create a nearly impenetrable fortress against tampering and fraud, making blockchain a powerful tool for secure digital interactions.

Cryptographic hashing, digital signatures, and other advanced techniques work together to ensure that once a transaction is recorded on the blockchain, it cannot be altered or forged. This unwavering security is what gives users the confidence to engage in digital transactions with a high level of trust.

Cryptographic Hashing and Data Integrity

Cryptographic hashing is a fundamental component of blockchain security. It involves using a one-way function—a mathematical algorithm—to transform any input data (a transaction in this case) into a unique, fixed-size string of characters called a hash. Even a tiny change to the input data results in a drastically different hash. This property is crucial for ensuring data integrity. If someone tries to alter a transaction after it’s been hashed, the resulting hash will be completely different, instantly revealing the tampering attempt. This mechanism effectively creates a digital fingerprint for each transaction, making any alteration immediately detectable. Common hashing algorithms used in blockchain include SHA-256 and SHA-3. For example, imagine a transaction detailing a transfer of 1 BTC. The hashing algorithm would convert all the data of this transaction (sender’s address, receiver’s address, amount, timestamp, etc.) into a unique hash. If even a single digit in the amount were changed, the hash would be completely different.

Digital Signatures and Transaction Authenticity

Digital signatures are another critical security element. They provide a way to verify the authenticity of a transaction and ensure that it originated from the claimed sender. These signatures are created using a pair of cryptographic keys: a private key (known only to the sender) and a public key (shared publicly). The sender uses their private key to sign the transaction, creating a digital signature. Anyone can then use the sender’s public key to verify this signature, confirming that the transaction was indeed signed by the owner of the private key. This process prevents forgery and ensures that only authorized individuals can initiate transactions. The security of digital signatures relies on the mathematical difficulty of deriving the private key from the public key. Elliptic Curve Digital Signature Algorithm (ECDSA) is a widely used algorithm for generating and verifying digital signatures in blockchain systems. For instance, when Alice sends Bob 0.5 ETH, she uses her private key to sign the transaction. Bob, or anyone else, can then use Alice’s public key to verify that the signature is valid, confirming that Alice initiated the transaction.

Examples of Cryptographic Techniques in Blockchain Security

Beyond hashing and digital signatures, numerous other cryptographic techniques contribute to blockchain security. These include:

- Merkle Trees: These data structures efficiently verify the integrity of large datasets by creating a hierarchical hash of all transactions within a block. This allows for verification of individual transactions without needing to download the entire blockchain.

- Proof-of-Work (PoW) and Proof-of-Stake (PoS): These consensus mechanisms use cryptography to secure the blockchain network by making it computationally expensive or economically unfavorable to attempt fraudulent activities.

- Zero-Knowledge Proofs (ZKPs): These advanced cryptographic techniques allow one party to prove to another that a statement is true without revealing any additional information. ZKPs are useful for enhancing privacy in blockchain transactions.

These cryptographic safeguards work in concert to create a secure and transparent system, building trust and confidence in blockchain-based transactions. The complexity and strength of these methods significantly raise the bar for potential attackers, ensuring the integrity and reliability of the blockchain.

Smart Contracts and Automated Trust

Source: ekoios.vn

Blockchain’s transparent, immutable ledger fosters trust in digital transactions, revolutionizing how we handle sensitive data. This increased security is further amplified by the scalability offered through cloud infrastructure, as explored in The Role of Cloud Computing in Scaling Global Businesses. Ultimately, the synergy between blockchain’s trust-building capabilities and cloud computing’s expansive reach ensures a more secure and efficient digital future for global commerce.

Imagine a world where agreements are self-executing, transparent, and virtually tamper-proof. That’s the promise of smart contracts, a revolutionary application of blockchain technology that’s transforming how we conduct business and build trust in the digital realm. They’re essentially self-enforcing contracts with the terms of the agreement written directly into lines of code and stored on a blockchain.

Smart contracts automate trust by eliminating the need for intermediaries to oversee and enforce agreements. Instead of relying on lawyers, notaries, or other third parties to verify and execute the terms of a contract, the blockchain itself acts as the guarantor, ensuring that the agreed-upon actions are carried out automatically upon the fulfillment of pre-defined conditions. This automated execution drastically reduces the risk of disputes and delays, leading to more efficient and reliable transactions.

Smart Contract Functionality

Smart contracts function by using conditional logic. The code defines specific triggers and outcomes. For example, if a certain event occurs (like a payment being received), a corresponding action is automatically executed (like the release of goods or services). This automation is achieved through the use of blockchain’s decentralized and immutable nature. Once deployed, the code cannot be altered, ensuring the integrity of the agreement. The transparency of the blockchain allows all parties involved to track the progress and status of the contract in real-time.

Industries Benefiting from Smart Contracts

The potential applications of smart contracts span numerous industries. Supply chain management, for instance, can leverage smart contracts to track goods as they move through the supply chain, ensuring authenticity and preventing counterfeiting. Each stage of the process, from origin to delivery, can be recorded on the blockchain, providing complete transparency and traceability. Imagine a shipment of pharmaceuticals; smart contracts can ensure that the temperature remains within acceptable ranges throughout transport, automatically triggering alerts if any deviation occurs.

Another sector seeing significant impact is the insurance industry. Smart contracts can automate claims processing, reducing processing time and costs. For example, a smart contract could automatically release a payout upon verification of a claim (like a car accident) using connected sensors and data from the involved vehicles. This eliminates the need for extensive paperwork and manual verification, speeding up the process and increasing customer satisfaction. Furthermore, the real estate industry is exploring smart contracts for secure and transparent property transactions, minimizing paperwork and streamlining the closing process.

Reduced Need for Intermediaries

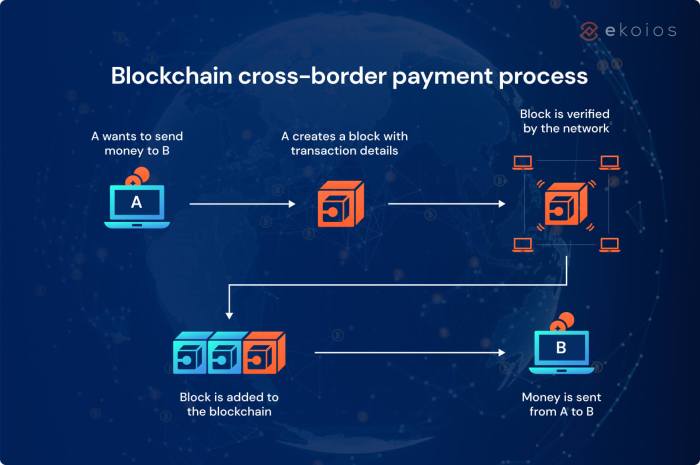

The decentralized nature of blockchain and the self-executing nature of smart contracts significantly reduce the reliance on intermediaries. Traditional transactions often involve multiple parties, each taking a cut and potentially introducing delays and inefficiencies. Smart contracts, however, automate many of these intermediary functions, cutting out the middlemen and streamlining the process. This results in cost savings, increased efficiency, and enhanced trust among parties involved. For example, in international trade, smart contracts can automate customs clearance processes, reducing delays and costs associated with handling documentation and approvals from multiple agencies. This efficiency boost is particularly crucial in cross-border transactions.

Blockchain’s Role in Supply Chain Management and Trust: How Blockchain Is Enabling Trust In Digital Transactions

Forget endless spreadsheets and confusing paperwork – blockchain is revolutionizing supply chain management, bringing a level of transparency and trust previously unimaginable. By creating a shared, immutable record of every transaction and movement within a supply chain, blockchain empowers businesses to track products from origin to consumer with unprecedented accuracy and efficiency. This, in turn, fosters stronger relationships with suppliers, enhances brand reputation, and ultimately boosts the bottom line.

Blockchain enhances traceability by creating a permanent, verifiable record of a product’s journey. Each step – from raw material sourcing to manufacturing, distribution, and retail – is recorded as a block on the blockchain. This detailed history is accessible to all authorized participants, providing complete visibility into the product’s provenance. This is a game-changer for industries with complex supply chains, like food and pharmaceuticals, where knowing the exact origin and handling of products is crucial for safety and quality assurance.

Enhanced Traceability in Supply Chains

Imagine a single, universally accessible ledger detailing the entire lifecycle of a coffee bean – from the farm in Colombia to the roasting facility in Seattle, and finally, to your local cafe. That’s the power of blockchain-enabled traceability. Each transaction, including the date, time, location, and even environmental conditions, is recorded and cryptographically secured, preventing tampering or falsification. This level of detail allows businesses to quickly identify and address potential issues, such as contaminated batches or supply chain disruptions, minimizing risk and maintaining consumer confidence. For example, Walmart utilizes blockchain to track the movement of its produce, enabling faster identification and removal of contaminated products from its shelves, protecting consumers and preserving its reputation.

Reduction of Counterfeiting in Supply Chains

Counterfeiting is a massive problem, costing businesses billions annually and jeopardizing consumer safety. Blockchain combats this by providing a tamper-proof record of authenticity. Each product can be assigned a unique digital identifier, linked to its verified origin and journey through the supply chain. This makes it virtually impossible to create convincing counterfeits, as any attempt to alter the blockchain record would be immediately detected. The luxury goods industry, particularly vulnerable to counterfeiting, is already exploring blockchain solutions to verify the authenticity of its products and combat the black market. A high-end handbag, for instance, could have its unique ID recorded on the blockchain from the moment the leather is sourced, ensuring its legitimacy throughout its journey to the consumer.

Improved Transparency and Accountability in Supply Chain Transactions

Blockchain fosters transparency by making information readily available to all authorized parties in the supply chain. This shared visibility promotes accountability, as every participant’s actions are recorded and auditable. This increased transparency builds trust among stakeholders, fostering stronger collaborations and streamlining processes. For instance, a company sourcing ethically produced cocoa beans can use blockchain to demonstrate the fair labor practices and environmental sustainability of its suppliers to its consumers, boosting its brand image and sales. This transparency allows for better monitoring of ethical sourcing, environmental impact, and fair trade practices throughout the entire supply chain.

Visual Representation of a Blockchain-Enabled Supply Chain

Imagine a flowchart. At the top, you see “Raw Materials Sourcing” – a block representing the origin of materials, with details like farm location and date harvested. Arrows point to the next block, “Manufacturing,” detailing the factory location, date of production, and any quality control checks. Another arrow leads to “Distribution,” showing the shipment details, including carrier, route, and arrival times. Finally, an arrow leads to “Retail,” showing the store location and date of sale. Each block is linked to the previous one via a cryptographic hash, creating an unbroken chain of information. Each block also contains a unique timestamp, making the sequence immutable and verifiable. All authorized parties in the supply chain – from farmers to retailers – have access to this shared, secure ledger, enabling them to track the product’s journey at any point in time. This clear, visual representation shows how every step is transparently recorded and easily auditable.

Challenges and Limitations of Blockchain for Trust

Source: trustkeys.network

While blockchain technology holds immense promise for revolutionizing trust in digital transactions, it’s not a silver bullet. Several challenges and limitations hinder its widespread adoption and impact on building complete trust. Understanding these hurdles is crucial for realistic expectations and informed development of blockchain-based solutions.

Scalability Issues

One major bottleneck for blockchain is scalability. Many existing blockchain networks struggle to process a high volume of transactions efficiently. This limitation stems from the inherent design of some blockchains, which require each node to validate every transaction, leading to slow processing speeds and high latency as the network grows. For example, Bitcoin, while secure, processes only a limited number of transactions per second compared to centralized payment systems like Visa. This constraint impacts the practicality of using blockchain for applications requiring high transaction throughput, such as real-time payment systems or high-frequency trading. Solutions being explored include sharding (dividing the blockchain into smaller, more manageable parts) and layer-2 scaling solutions (processing transactions off-chain and settling them on the main chain periodically).

Regulatory Hurdles

The decentralized and often pseudonymous nature of blockchain presents regulatory challenges for governments worldwide. The lack of clear regulatory frameworks for cryptocurrencies and blockchain-based applications creates uncertainty for businesses and investors. Issues like taxation of cryptocurrency transactions, anti-money laundering (AML) compliance, and data privacy regulations vary significantly across jurisdictions, creating fragmentation and hindering cross-border adoption. For instance, the differing regulatory approaches to Initial Coin Offerings (ICOs) across various countries have led to confusion and legal battles. The ongoing development of clear, consistent, and internationally harmonized regulatory frameworks is essential for the wider acceptance of blockchain technology.

Potential Solutions to Address Limitations

Addressing the challenges facing blockchain requires a multi-pronged approach. Improvements in blockchain architecture, such as the development of more scalable consensus mechanisms and the use of layer-2 solutions, are actively being pursued. Furthermore, increased collaboration between blockchain developers, regulators, and industry stakeholders is vital for establishing clear regulatory guidelines that foster innovation while mitigating risks. This includes developing standardized KYC/AML procedures for blockchain platforms and promoting interoperability between different blockchain networks to enable seamless data exchange and transaction processing. Ultimately, a collaborative effort is necessary to unlock the full potential of blockchain while mitigating its inherent limitations.

Epilogue

In a world increasingly reliant on digital interactions, the need for trust is paramount. Blockchain technology, with its inherent security and transparency, is emerging as a powerful solution. While challenges remain, the potential of blockchain to revolutionize how we conduct digital transactions is undeniable. From streamlining supply chains to securing online payments, blockchain’s impact is only going to grow, ushering in an era of unprecedented trust and efficiency in the digital realm. It’s not just about the technology; it’s about building a more trustworthy future, one block at a time.